Global financial markets enter the week near record highs, but investor sentiment is likely to be tested by a combination of inflation data, central bank expectations, geopolitical developments, and key corporate earnings. After a strong rally led by technology and AI-related stocks, markets now face an important macroeconomic reality check.

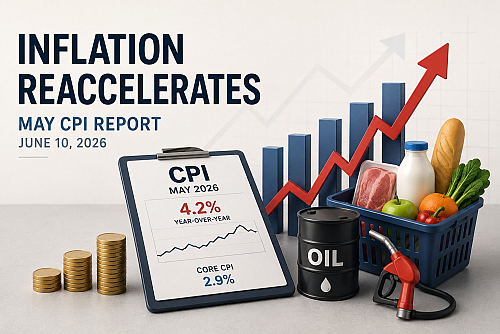

The main focus this week will be inflation. In the United States, the April Consumer Price Index (CPI) report is expected to show renewed price pressures, partly driven by higher energy prices and ongoing geopolitical tensions in the Middle East. Markets will closely monitor whether inflation remains sticky enough to delay future Federal Reserve rate cuts. A stronger-than-expected CPI reading could push bond yields higher and increase volatility across equity markets.

Alongside CPI, investors will also watch the Producer Price Index (PPI), retail sales data, and weekly jobless claims. Retail sales will provide an important indication of the strength of the U.S. consumer, especially as higher oil prices begin to pressure household spending. Economic resilience has supported equities so far, but any signs of weakening demand could trigger concerns about slower growth ahead.

Central bank communication remains another major theme. Several Federal Reserve officials are scheduled to speak during the week, and markets continue to reassess the outlook for interest rates after stronger economic data and persistent inflation. Investors are also monitoring developments surrounding the future leadership of the Federal Reserve, which could influence longer-term policy expectations.

Geopolitical risks are also back in focus. Tensions involving Iran and uncertainty around U.S.-China relations continue to influence oil prices and overall market sentiment. Crude oil prices have risen sharply in recent sessions, increasing concerns about inflationary pressure and the broader impact on global growth. Energy markets could remain highly volatile depending on diplomatic developments during the week.

On the corporate side, investors will closely follow earnings from major technology, semiconductor, retail, and AI-related companies. Results and guidance from companies exposed to artificial intelligence infrastructure and consumer spending trends will be particularly important for market direction. Firms such as Cisco Systems, Applied Materials, and Walmart are expected to provide valuable insight into enterprise spending, AI investment momentum, and consumer behaviour.

Technology stocks continue to lead the broader market rally, particularly semiconductor and artificial intelligence companies. Investors remain highly focused on demand trends in AI infrastructure, which has become one of the strongest themes driving equity markets in 2026. NVIDIA remains at the center of market attention as optimism around AI spending continues to support valuations across the technology sector.

In Europe, investors will monitor inflation figures, industrial production data, and GDP releases from major economies, including the UK and the Eurozone. European markets remain sensitive to global trade dynamics, energy prices, and ECB policy expectations.

Overall, this week could prove decisive for short-term market direction. If inflation data surprises to the upside, markets may begin pricing in a “higher-for-longer” interest rate environment again. However, resilient economic growth and continued strength in corporate earnings could help support risk appetite despite rising macroeconomic uncertainty.