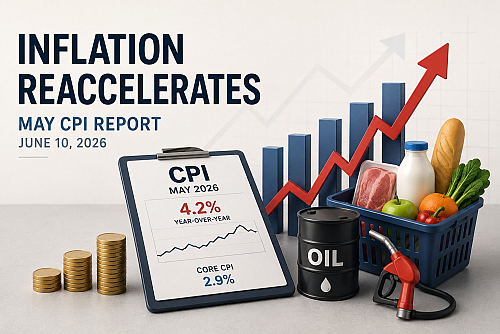

The latest U.S. inflation report released on May 12 showed that price pressures remain a major concern for both consumers and financial markets. According to the April Consumer Price Index (CPI) data, annual inflation accelerated to 3.8%, up from 3.3% in March, marking the highest reading since mid-2023.

The main driver behind the renewed inflation surge was energy. Rising geopolitical tensions in the Middle East and disruptions in oil supply chains pushed gasoline prices sharply higher during April. Energy prices rose 17.9% year-over-year, while gasoline alone jumped more than 28% compared with the same period last year.

However, the report also showed that inflationary pressures are no longer limited to fuel. Core inflation, which excludes food and energy, climbed to 2.8%, slightly above expectations. Shelter costs, airline fares, household goods, and apparel all contributed to the increase, suggesting that higher energy prices are beginning to spread through the broader economy.

For financial markets, the inflation data complicates the outlook for the Federal Reserve. Investors had been hoping for potential interest rate cuts later this year, but persistently elevated inflation may force policymakers to maintain restrictive monetary conditions for longer. Treasury yields moved higher following the report, while equity markets reacted cautiously as investors reassessed expectations for monetary policy.

The report also highlights growing pressure on household purchasing power. Although wages continue to rise, inflation is once again eroding real income growth, particularly for middle-income consumers facing higher transportation, utility, and grocery bills.

Looking ahead, markets will closely monitor upcoming producer price and consumer spending data to determine whether April’s inflation jump was temporary or the beginning of a broader second wave of price pressures. Much will depend on energy markets and geopolitical developments over the coming months.