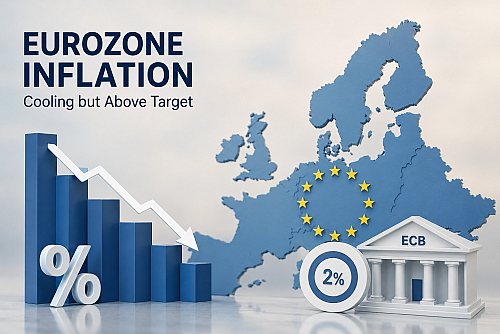

Inflation across Europe remains a key concern for policymakers and investors, with the latest data showing that price pressures are still running above the European Central Bank’s (ECB) 2% target. The Eurozone’s annual inflation rate reached 3.0% in April 2026, the highest level since September 2023, highlighting the persistence of inflation despite earlier signs of moderation.

A major driver of the recent increase has been the sharp rise in energy prices. Eurozone energy inflation surged by 10.8% year-on-year, largely due to supply concerns linked to geopolitical tensions in the Middle East and higher oil prices. Food prices have also continued to rise, while inflation in industrial goods accelerated modestly.

Among Europe’s largest economies, inflation remains uneven. Spain recorded inflation of 3.5% in April, while Germany reached 2.9%, Italy 2.8%, and France 2.5%. More recent preliminary data for May suggest inflationary pressures remain elevated, with Spain’s harmonised inflation rate climbing to 3.6%, and France and Italy also reporting stronger price growth.

There is, however, some encouraging news beneath the headline figures. Core inflation, which excludes volatile food and energy prices, eased to 2.2%, indicating that underlying inflationary pressures are not accelerating at the same pace as energy-driven costs. This suggests that much of the recent inflation surge is linked to external supply shocks rather than broad-based overheating in the economy.

For the ECB, the challenge remains balancing inflation control with economic growth. While higher energy prices could keep inflation above target in the coming months, policymakers will be closely watching whether core inflation continues to moderate before considering further monetary tightening. Analysts expect inflation to remain volatile throughout the summer, particularly if geopolitical tensions continue to affect global energy markets.