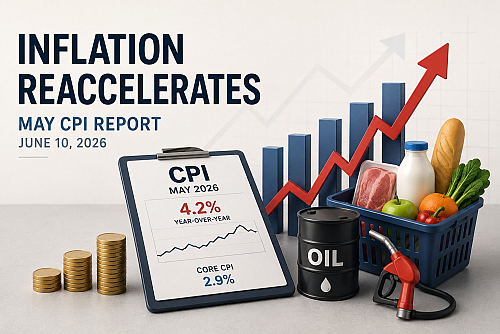

The latest U.S. Consumer Price Index (CPI) report, released on 14 July 2026, delivered welcome news for financial markets. Inflation eased more than economists had expected, reinforcing hopes that price pressures are gradually coming under control and reducing the likelihood of another near-term interest rate increase from the Federal Reserve.

Headline CPI rose 3.5% year-over-year in June, down from 4.2% in May, while consumer prices fell 0.4% from the previous month, the first monthly decline since 2020. Core inflation, which excludes volatile food and energy prices, slowed to 2.6% annually and was unchanged on a monthly basis. The primary driver of the improvement was a sharp decline in gasoline and broader energy prices, following the easing of energy market disruptions during June.

Financial Markets React Positively

Investors welcomed the softer inflation data, interpreting it as a sign that the Federal Reserve may be able to keep interest rates unchanged at its upcoming meeting.

Following the report:

• U.S. equities moved higher, with gains led by technology and growth stocks.

• Treasury yields declined as investors priced in lower expectations for additional rate hikes.

• The U.S. dollar weakened against major currencies as interest rate expectations eased.

• Market participants increased expectations that monetary policy could become less restrictive if inflation continues to moderate.

What Investors Should Watch Next

While the June CPI report is encouraging, inflation remains above the Federal Reserve's long-term 2% target. Policymakers are therefore likely to remain cautious, particularly given ongoing geopolitical tensions and the possibility that energy prices could rebound in the coming months.

Investors will now closely monitor upcoming inflation reports, labor market data, and corporate earnings to determine whether the recent improvement represents the beginning of a sustained disinflation trend or merely temporary relief driven by lower energy costs.

For long-term investors, the latest data supports a more constructive outlook for financial markets, although diversification and disciplined portfolio management remain essential in an environment where inflation risks have not disappeared entirely.