On March 19, 2026, the world’s major central banks- the ECB, Federal Reserve, Bank of England, and Swiss National Bank- delivered a synchronized message: hold rates steady, but remain highly vigilant.

Despite different domestic conditions, policymakers are now aligned around a common challenge, renewed inflation risks driven by the Middle East conflict and energy price shock.

A Coordinated Pause Across Major Economies

• European Central Bank (ECB)

The ECB held its key rate at 2.0%, maintaining a wait-and-see stance. While inflation had recently eased toward target, policymakers warned that surging energy prices could push inflation higher again, revising 2026 projections upward.

• Federal Reserve (Fed)

The Fed kept rates unchanged at 3.50%–3.75%, signaling caution. While the base case still includes gradual easing over the coming years, the current environment, especially energy-driven inflation, justifies patience.

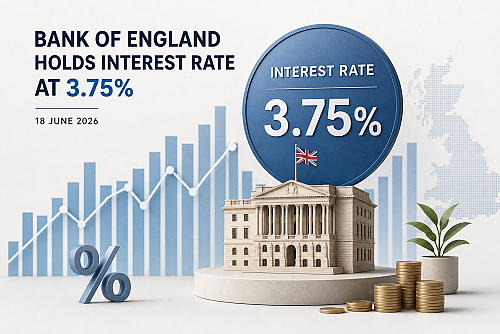

• Bank of England (BoE)

The BoE also held at 3.75%, in a unanimous decision. However, its tone was notably more hawkish, warning that inflation could reaccelerate toward ~3.5%, with markets now pricing potential rate hikes later in 2026.

• Swiss National Bank (SNB)

The SNB maintained its policy rate at 0%, reflecting Switzerland’s lower inflation environment. Instead of tightening, it signaled readiness to intervene in FX markets to prevent excessive Swiss franc strength.

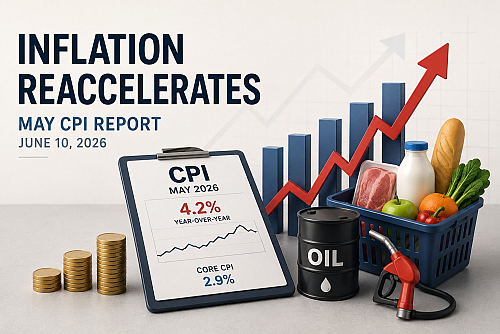

The Key Driver: Energy Shock and Inflation Uncertainty

Across all four institutions, one factor dominates the policy narrative:

The inflationary impact of rising oil and gas prices is linked to geopolitical tensions.

• Oil prices briefly surged above $100–$119 per barrel

• European gas prices spiked sharply

• Inflation forecasts are being revised upward again

This creates a policy dilemma:

• Tighten too early → risk slowing already fragile growth

• Ease too soon → risk reigniting inflation

Market Implications: From Cuts to Potential Hikes

Only weeks ago, markets expected rate cuts in 2026.

Now, the narrative is shifting:

• Fewer or delayed cuts from the Fed

• Possible hikes from the BoE and ECB later this year

• Increased volatility in FX and rates markets

This repricing reflects a broader shift toward a “higher-for-longer, with upside risks” scenario.

Bottom Line

The March 19 decisions mark a turning point:

Central banks are no longer confidently moving toward easing; instead, they are re-entering a defensive stance.

For investors, this reinforces three themes:

1. Policy uncertainty is back

2. Inflation is not fully defeated

3. Geopolitics is once again a key macro driver