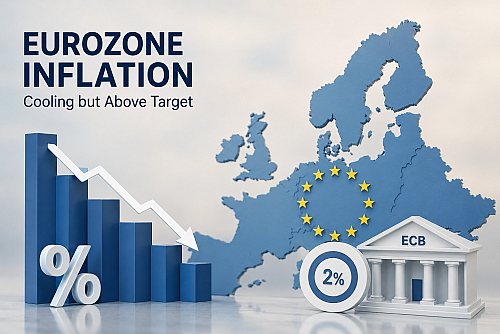

This week, Eurostat data showed that inflation in the Eurozone ticked up slightly in November, rising from 2.1% to 2.2% year-on-year. That increase, though small, matters because it keeps inflation firmly above the target set by the European Central Bank (ECB). The uptick suggests that, despite lower energy prices, underlying price pressures remain present elsewhere.

In particular, “core” inflation, which excludes volatile items such as energy and unprocessed food, held at around 2.4 %, underscoring persistent domestic inflation dynamics. Likewise, service-sector inflation was a key driver: service prices increased by roughly 3.5 %, the highest such reading since April, pointing to sustained cost pressures in non-energy sectors.

Why this matters for monetary policy

For the ECB, stability around the 2 % mark is generally the “sweet spot.” Moderately above target, inflation suggests the economy is neither overheating nor sliding into deflation.

Given the data, markets now broadly expect that the ECB will hold interest rates steady at its next meeting (scheduled for December 18, 2025). In practical terms, that means the modest inflation rise reduces the likelihood of a near-term rate cut, a scenario previously debated if inflation had fallen significantly below target.

What’s holding up inflation, and what’s cooling it

Supporting inflation:

• Services: The 3.5 % increase in service price inflation is a major factor. Rising costs in housing, leisure, hospitality, and other service sectors, possibly driven by wage pressures, rent increases, or strong demand, are exerting upward pressure.

• Non-energy goods/core inflation: With core inflation at 2.4 %, we see that price pressures go beyond volatile energy or food segments. That suggests relatively broad-based inflation rather than a narrow spike.

Cooling factors:

• Energy prices: These have dropped compared with previous periods, providing a downward drag on headline inflation. Technically, declining energy costs help keep the overall index from rising more sharply.

• Goods inflation: Some categories (especially durable goods or non-service goods) appear less inflationary, which helps prevent inflation from accelerating out of control.

Risks and implications, what to watch out for

• Sticky services inflation: As long as services inflation remains elevated, overall inflation could remain above target even if energy and goods prices are stable. This makes the inflation “baseline” more persistent.

• Wage-price dynamics: If wages continue to rise, especially in sectors with tight labor markets, upward pressure on services and rental prices could further entrench inflation.

• Policy drift/rate expectations: With inflation above 2 %, the ECB may avoid rate cuts for the foreseeable future, but that limits flexibility if economic growth slows or external shocks hit (e.g., energy markets, global demand).

• Uncertainty around goods deflation vs. service inflation: Diverging price trends across sectors can complicate economic forecasts and asset-pricing models, which may affect investors’ and banks’ strategies.

What’s next and what to monitor

• The December ECB meeting: Will the ECB reiterate its “wait-and-see” stance? Or hint at further action if inflation remains sticky?

• Evolution of wage growth and services-sector pricing: These will largely determine whether inflation stays at 2 % or drifts higher.

• Energy-price developments: A renewed increase in energy costs would push headline inflation up again, with knock-on effects on core inflation and expectations.

• Real economy signals: Growth, consumer spending, corporate margins all will influence how sustainable inflation trends are and how monetary policy evolves.

The recent uptick in euro-zone inflation to 2.2 %, driven by strong services-sector price growth and maintained core inflation, reflects a nuanced backdrop. While declining energy costs offer some relief, persistent domestic price pressures may keep inflation anchored above the target for some time.

For investors, the environment calls for careful allocation and protection of real value: fixed-income instruments need to be balanced against real assets, and inflation hedges may regain importance.

At the same time, monetary policy appears set to remain cautious, meaning interest-rate moves are unlikely in the near term, but the unpredictable interplay of wages, energy costs, and global economic conditions means vigilance remains essential.